Imagine driving home on a rainy evening. Suddenly, another car slides into yours. Everyone walks away safe, but your vehicle is completely destroyed. Later, your insurance company delivers the bad news: your vehicle is a total loss. Now, you face a major question about your auto insurance policy. How exactly will the company calculate your payout?

When a vehicle is totaled, car insurance companies use two main methods to pay out claims. These two options are Actual Cash Value (ACV) and Replacement Cost. Understanding these terms helps you choose the right coverage ahead of time and avoids nasty surprises during a claim.

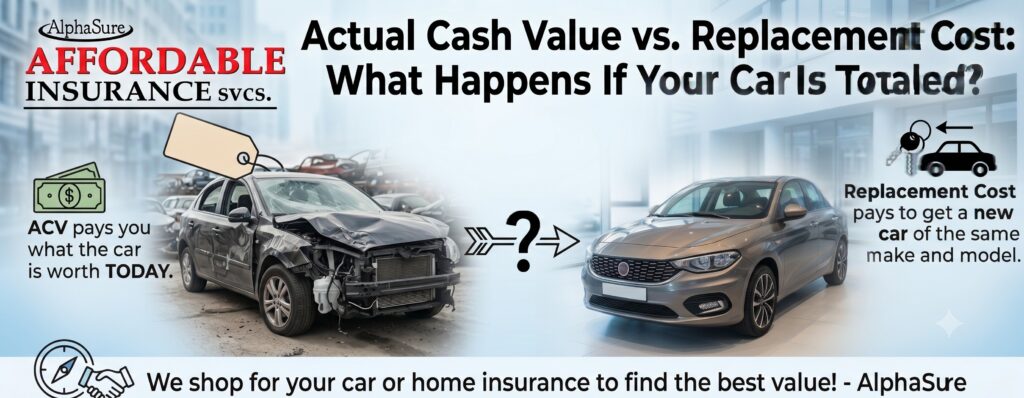

What is Actual Cash Value (ACV) in Auto Insurance?

Actual Cash Value is the standard option for most basic auto insurance policies. Essentially, ACV pays you exactly what your car was worth right before the accident occurred.

To find this specific number, the auto insurance company looks at the original purchase price of your vehicle. Then, they subtract depreciation. Depreciation is the natural loss of value over time due to normal wear and tear. For example, if you bought a car for $30,000 five years ago, it might only be worth $15,000 today. Therefore, under an ACV policy, $15,000 less any deductible is the final check amount you would receive.

What is Replacement Cost Coverage?

Replacement Cost coverage works quite differently. Instead of looking at current market value, it pays to buy a brand-new car of the exact same make and model. Crucially, this option does not subtract any money for depreciation.

Consequently, if your five-year-old car is totaled, a replacement cost policy pays for a current, brand-new version of that vehicle. This coverage gives you complete peace of mind after an accident. However, it comes with a major catch. Replacement cost coverage is very rare for standard auto insurance and usually costs much more. In fact, most companies only offer it for brand-new cars during their first year of ownership.

Why the Difference Matters to Your Auto Insurance Premium

The gap between ACV and Replacement Cost can be an impact to your financial health. For instance, cars lose value very quickly. In reality, a brand-new vehicle loses about twenty percent of its total value in the first twelve months alone.

If you have an ACV policy and still owe money on your vehicle, you might face a serious problem. Your insurance payout might be thousands of dollars less than what you still owe on your vehicle loan. This stressful situation leaves you paying off a loan for a car you can no longer drive. In this instance, buying a gap insurance policy at the dealership is highly advisable.

How a Local Independent Auto Insurance Agent Can Help

Choosing the right auto insurance policy can feel overwhelming. Fortunately, you do not have to shop for coverage alone. A local independent agent like AlphaSure Affordable Insurance Services can guide you through the process seamlessly.

Independent agents do not work for just one specific insurance company. Instead, they work with many! Thus, they compare rates from many different providers to find the best deals. Additionally, AlphaSure Affordable Insurance Services can help you shop for car or home insurance at the same time.

Final Thoughts on Choosing Your Policy Getting the right insurance policy can protect your finances from sudden disasters. Always review your options carefully before you sign a new contract. If you live in Texas, call AlphaSure Affordable Insurance Services today to get an home or auto insurance quote. If you prefer an in-person visit, come by our local Laredo or San Antonio, TX office.