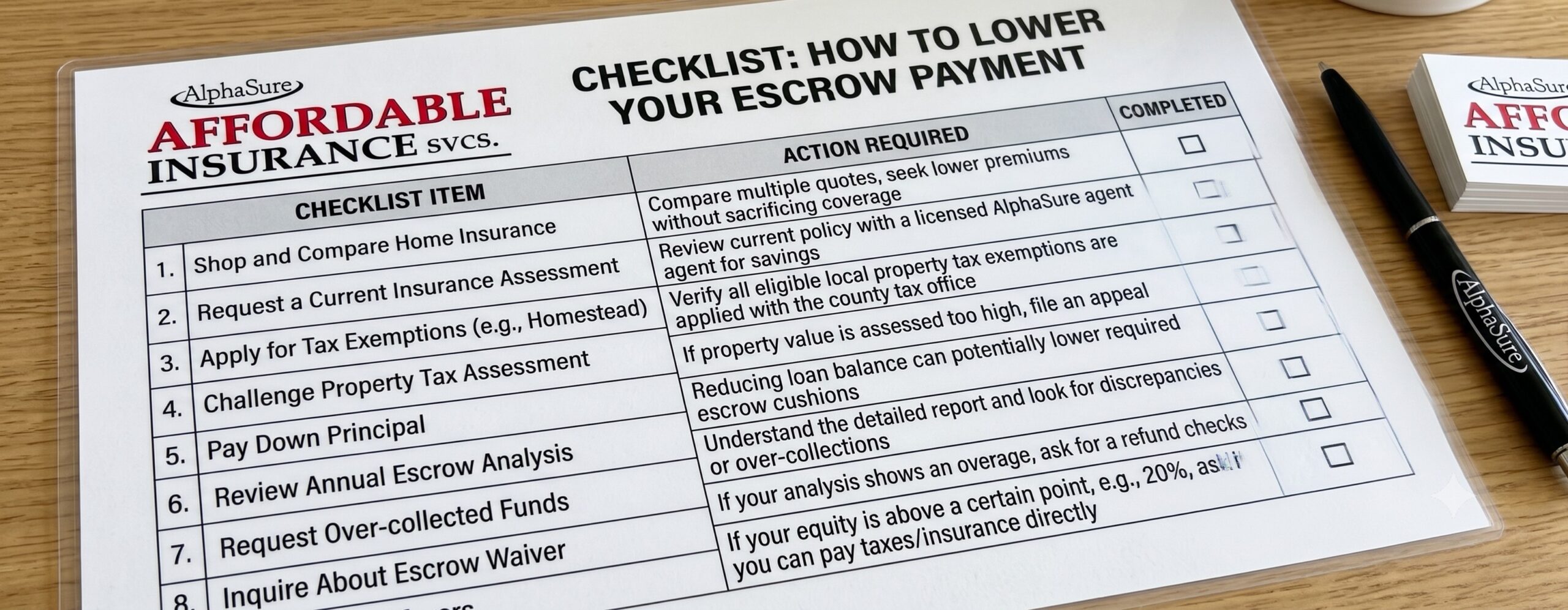

Why Did My Fixed Mortgage Payment Go Up? It could be because of the home insurance.

Have you ever opened your monthly mortgage statement and received a shocking surprise? Your monthly payment went up, but you have a fixed interest rate. How can that happen? A fixed-rate loan means your principal and interest payments never change. Therefore, if your total payment increased, it means either your home insurance or your property taxes (or both!) went up.

Most home loans use an escrow account. Your lender collects extra money each month to pay your annual tax and home insurance bills. When these bills rise, your escrow account falls short, and your lender raises your monthly payment to cover the gap.

The Good News about Shopping for Home Insurance

If a rising insurance premium caused your higher payment, you have options. Many homeowners believe they must wait until their current policy expires to switch companies. This is a myth! You can shop for new home insurance at any time.

Consequently, if you find a better home insurance rate, you can switch immediately. Your old insurance company will refund the unused portion of your premium on a prorated basis. Thus, that refund goes right back into your pocket or your escrow account, helping lower your costs.

💡 Smart Shopper Tip: Check Your Homestead Exemption

Before you change anything, check your property tax status. If you live in the home as your primary residence, make sure you have filed for a homestead exemption with your county tax office. This special tax exemption can lower your home’s taxable value and cap how much your property taxes can rise each year. It is a quick step that saves hundreds of dollars annually.

Work with a Local Independent Home Insurance Agent

Shopping for home insurance on your own can feel overwhelming and take hours. Instead, work with a local independent insurance agent like AlphaSure Affordable Insurance Services. Independent agents do not work for just one big insurance company. Instead, they compare quotes from several top-rated providers.

Don’t let a rising mortgage payment ruin your budget. Check your tax exemptions today and reach out to a local independent agent to start saving on your home insurance.

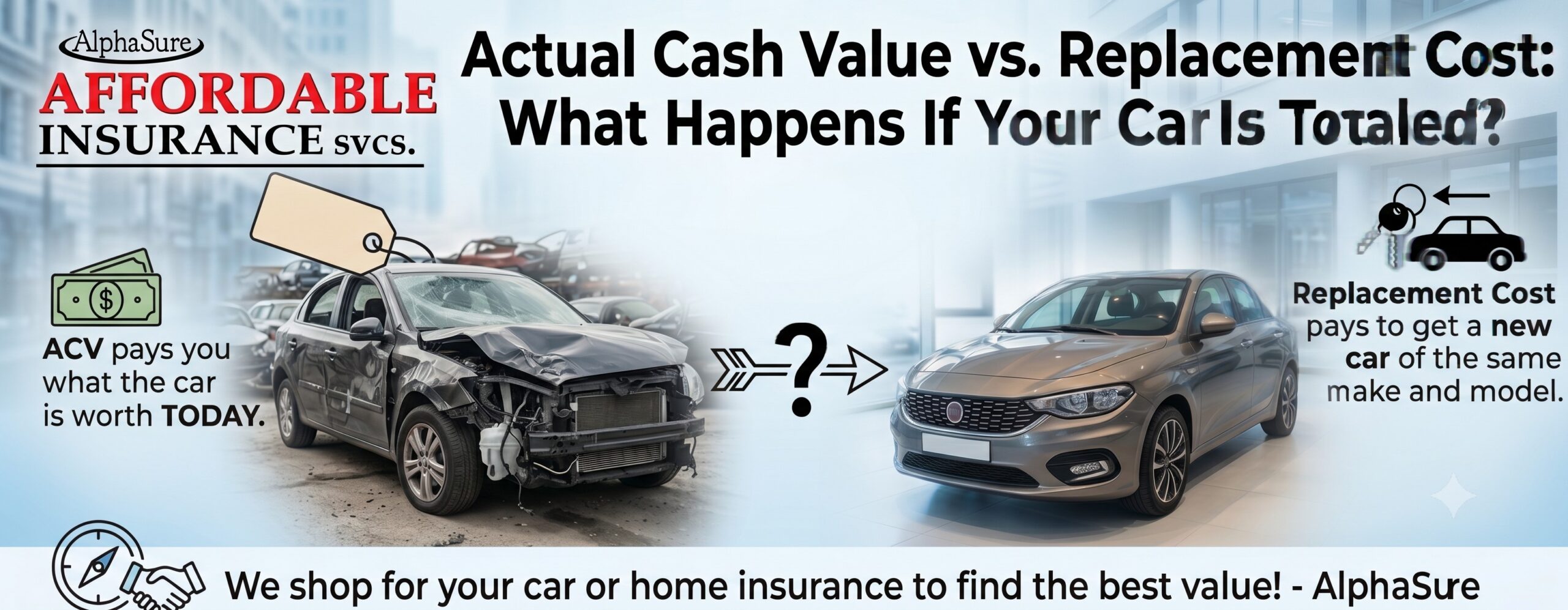

Imagine driving home on a rainy evening. Suddenly, another car slides into yours. Everyone walks away safe, but your vehicle is completely destroyed. Later, your insurance company delivers the bad news: your vehicle is a total loss. Now, you face a major question about your auto insurance policy. How exactly will the company calculate your payout?

When a vehicle is totaled, car insurance companies use two main methods to pay out claims. These two options are Actual Cash Value (ACV) and Replacement Cost. Understanding these terms helps you choose the right coverage ahead of time and avoids nasty surprises during a claim.

What is Actual Cash Value (ACV) in Auto Insurance?

Actual Cash Value is the standard option for most basic auto insurance policies. Essentially, ACV pays you exactly what your car was worth right before the accident occurred.

To find this specific number, the auto insurance company looks at the original purchase price of your vehicle. Then, they subtract depreciation. Depreciation is the natural loss of value over time due to normal wear and tear. For example, if you bought a car for $30,000 five years ago, it might only be worth $15,000 today. Therefore, under an ACV policy, $15,000 less any deductible is the final check amount you would receive.

What is Replacement Cost Coverage?

Replacement Cost coverage works quite differently. Instead of looking at current market value, it pays to buy a brand-new car of the exact same make and model. Crucially, this option does not subtract any money for depreciation.

Consequently, if your five-year-old car is totaled, a replacement cost policy pays for a current, brand-new version of that vehicle. This coverage gives you complete peace of mind after an accident. However, it comes with a major catch. Replacement cost coverage is very rare for standard auto insurance and usually costs much more. In fact, most companies only offer it for brand-new cars during their first year of ownership.

Why the Difference Matters to Your Auto Insurance Premium

The gap between ACV and Replacement Cost can be an impact to your financial health. For instance, cars lose value very quickly. In reality, a brand-new vehicle loses about twenty percent of its total value in the first twelve months alone.

If you have an ACV policy and still owe money on your vehicle, you might face a serious problem. Your insurance payout might be thousands of dollars less than what you still owe on your vehicle loan. This stressful situation leaves you paying off a loan for a car you can no longer drive. In this instance, buying a gap insurance policy at the dealership is highly advisable.

How a Local Independent Auto Insurance Agent Can Help

Choosing the right auto insurance policy can feel overwhelming. Fortunately, you do not have to shop for coverage alone. A local independent agent like AlphaSure Affordable Insurance Services can guide you through the process seamlessly.

Independent agents do not work for just one specific insurance company. Instead, they work with many! Thus, they compare rates from many different providers to find the best deals. Additionally, AlphaSure Affordable Insurance Services can help you shop for car or home insurance at the same time.

Final Thoughts on Choosing Your Policy Getting the right insurance policy can protect your finances from sudden disasters. Always review your options carefully before you sign a new contract. If you live in Texas, call AlphaSure Affordable Insurance Services today to get an home or auto insurance quote. If you prefer an in-person visit, come by our local Laredo or San Antonio, TX office.

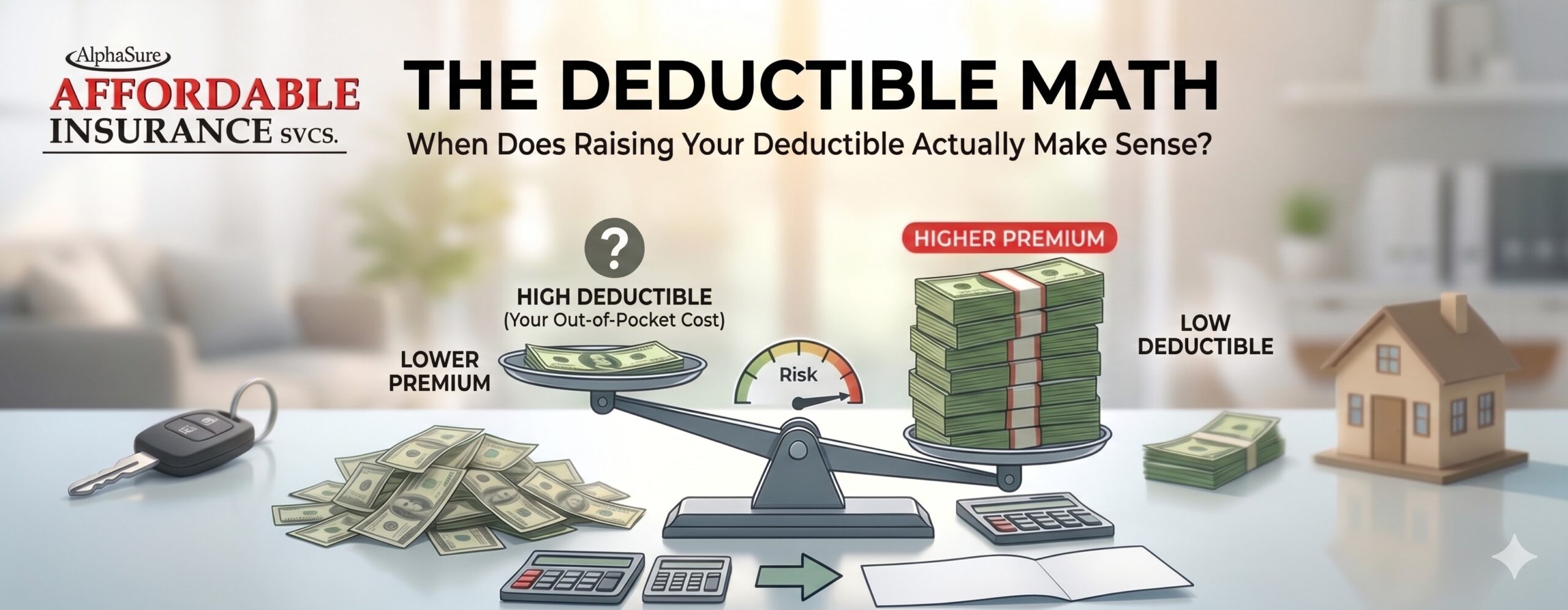

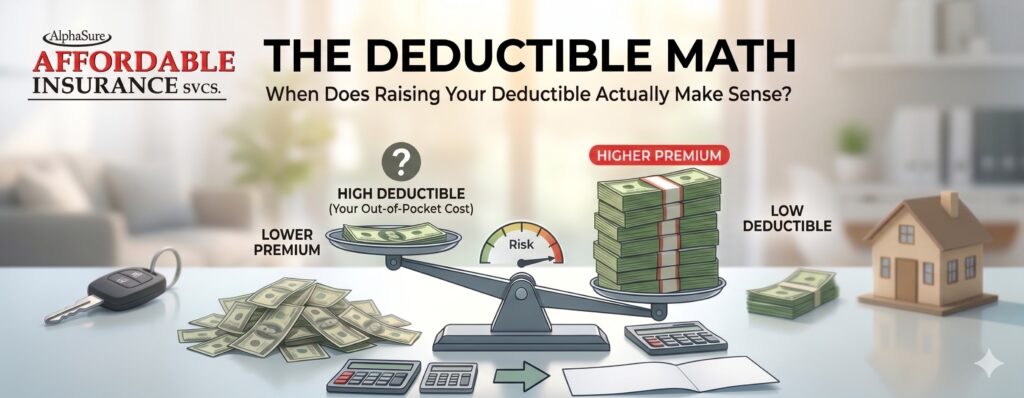

Choosing a car insurance policy can feel like a big puzzle. You want great coverage, but you also want a lower monthly payment. One common method to save money is raising your deductible. But when does this financial move actually make sense? Let’s break down the math in plain English so you can make an educated choice for your wallet.

What is a Car Insurance Deductible?

A car insurance deductible is an amount applied to covered comprehensive or collision claims. Essentially, you will be responsible to pay the deductible out of pocket before your insurance company pays for damages due to a covered claim. For example, imagine you get into a minor fender bender. The vehicle repairs cost $1,200. If your deductible is $500, you pay $500 first, and your insurance covers the remaining $700.

The Basic Math: Premium vs. Deductible

Insurance companies follow a simple rule: when your deductible goes up, your monthly premium goes down. This happens because you take on more of the initial financial risk. If you raise your deductible from $250 to $1,000, your car insurance premium drops. However, you must consider that in the event of a covered claim you will need to be ready with $1,000 to pay for the deductible.

When Does Raising the Car Insurance Deductible Make Sense?

First, examine your personal savings. Raising your deductible only works if you can pay that higher deductible amount tomorrow without stress. If an unexpected $1,000 expense ruins your budget, then it may be better to keep a lower deductible for now.

Second, think about your driving history and habits. Have you gone many years without an accident? Do you drive a safe route? If your risk of making a claim is low, a higher deductible can save you hundreds of dollars each year.

Third, do a quick math calculation. Suppose raising your deductible saves you $150 a year on car insurance. If you go more than five years without a claim, you have saved $750. Conceivably, that savings can offset the cost of the deductible if you ever get into a crash.

How a Local Independent Car Insurance Agent Helps

You do not have to calculate these numbers by yourself. Shopping for car insurance can get overwhelming quickly. That is why working with a local independent insurance agent like AlphaSure Affordable Insurance Services is a smart move.

Unlike brand agents who only sell one product, independent agents shop around with many different companies. Therefore, they find the best rates and coverage options for your budget. They can run the numbers for you to show exactly how much you will save by changing your deductible. Plus, they understand your local community and can provide personalized advice.

Final Thoughts

Raising your deductible is a proven way to lower your insurance costs. However, you should only do it if you have a solid emergency fund. Talk to the experts at AlphaSure Affordable Insurance Services today to find the car insurance plan that you can live with.

Have you ever thought about letting your car insurance coverage “pause” for a few weeks? Maybe you are between vehicles right now. Or perhaps you just want to save a quick buck this month. However, you should think twice before you make that choice.

A gap in your auto policy is called a coverage lapse. It might seem harmless at first glance, but it may cost you more in the long run. These unexpected costs can hurt your wallet for many years to come.

Fortunately, you can avoid these financial traps easily. Let us look at why keeping your policy active matters so much, and how an independent agency can protect your budget.

The Hidden Costs of a Car Insurance Coverage Lapse (And How to Avoid One)

The Real Price of a Car Insurance Gap

1. Your Premium Rates Will Increase

Insurance companies view drivers with a coverage gap as high-risk clients. Consequently, when you finally buy a new policy, companies will charge you a much higher premium. This is because, you will lose your “continuous insurance” discount. Thus, depending on the insurance company, a few days can double your future car insurance rates.

2. You Will Pay Heavy Legal Fines

In Texas, the TexasSure program keeps a database of insured vehicles. As a result, there some jurisdictions in Texas that actively seek to fine and tow uninsured vehicles. This will lead to fines and inconveniences that could have been avoided.

3. You Face High Out-of-Pocket Expenses

Accidents always happen when you least expect them. If you cause a crash during an insurance lapse, you must pay for all vehicle repairs out of your own pocket. Furthermore, you have to cover medical bills for anyone you may have injured. As a result, you can find yourself in a lawsuit. This single mistake can easily lead to complete financial ruin.

How to Safely Avoid a Car Insurance Coverage Lapse

You never have to suffer through these high costs. Instead, you can follow these simple steps to protect your household budget:

Use Non-Owner Car Insurance: If you sell your vehicle but plan to buy another one soon, get a non-owner policy. This special car insurance policy keeps your insurance history clean and keeps your future rates low.

Set Up Auto-Pay: Avoid accidental cancellations by letting your bank handle your monthly payments automatically.

Plan Your Timing Ahead: Never cancel an old policy until your new car insurance policy is active.

Let a Local Car Insurance Professional Do the Work

Shopping for car insurance coverage alone feels overwhelming. Fortunately, you do not have to do it by yourself. A local independent agent can find the best deals for your specific situation.

AlphaSure Affordable Insurance Services helps local drivers search the insurance market. Because they are independent, AlphaSure can compare multiple top companies at once. They work hard to find cheap car insurance or home insurance without sacrificing your protection.

Call a local independent insurance agent today to keep your record clean, avoid lapses, and save your hard-earned money.

Why DOT and FMCSA Status Changes Can Affect Trucking Liability Coverage

For trucking businesses based in San Antonio, TX, changes to DOT or FMCSA status are more than administrative updates. They can directly impact how trucking liability insurance responds in the event of an accident. AlphaSure Affordable Insurance Services works closely with owner-operators and fleets to help ensure liability coverage stays aligned when regulatory status changes occur.

New Authority and Reinstatement Create New Exposure

When a carrier receives new operating authority or reinstates an inactive DOT number, insurers often view the operation as higher risk until a new compliance history is established. Trucking liability coverage may need to be reviewed to confirm limits, filings, and endorsements match the carrier’s current authority. Overlooking this step can lead to filing issues or claim delays.

Operating Radius Changes Affect Liability Risk

Expanding from local routes to regional or interstate hauling changes the scope of exposure. Longer routes increase time on the road, traffic density, and accident severity potential. Trucking liability policies are structured around operating radius, and coverage should reflect how far and where vehicles are traveling after FMCSA updates.

Vehicle and Driver Updates Trigger Review Needs

DOT status changes often occur alongside fleet growth or driver additions. New power units, trailers, or drivers can affect liability exposure and compliance filings. If policies are not updated to reflect these operational changes, gaps can appear between what is reported to regulators and what is insured.

Compliance Filings Must Match Active Operations

FMCSA and state filings such as MCS-90 endorsements rely on accurate insurance information. If authority status changes but insurance filings are outdated, carriers may face compliance violations or complications during inspections. A trucking liability review ensures filings align with active operations.

Local Expertise Helps Keep Coverage in Sync

Trucking regulations change quickly, and insurance should keep pace. AlphaSure Affordable Insurance Services in San Antonio, TX helps trucking professionals review liability coverage after DOT or FMCSA status changes to reduce compliance risk and claim uncertainty. To learn more about aligning your trucking liability coverage with your operating authority, visit the AlphaSure Affordable Insurance Services website.

Have you looked out at your yard lately? If you see large tree branches hanging over your roofline, it might be time to hire a tree trimmer. In Texas, keeping your trees neat is not just about curb appeal, it also plays a huge role in your home insurance eligibility and possibly, your wallet.

Trimming tree branches away from your roofline drastically improves your home insurance eligibility. In fact, it might even help you find a lower priced home policy.

Texas Home Insurance Companies Care About Your Trees

Texas weather is highly unpredictable. From intense windstorms and heavy hail to hurricanes, our homes take a beating every year. Thus, when severe weather hits, overgrown branches become major hazards.

First, strong winds can snap heavy limbs, sending them crashing directly into your roof. This causes severe structural destruction and expensive leaks. Second, constant rubbing from nearby branches can scrape away the protective granules on your roof shingles over time. This mechanical friction weakens your roof long before a storm even arrives. Finally, overhanging branches drop leaves and twigs that clog your gutters, leading to rot and water damage.

The Eye in the Sky: How Home Insurance Companies Spot Overgrown Trees

You might think an insurance company will only notice your trees if you file a claim, but that is no longer the case. Today, technology allows providers to view your property from above.

Many insurance companies now use high-resolution satellite images and aerial photography via drones to review your roof layout. Sometimes, they use these images to check the condition of your home before they even agree to cover your home. Thus, the number of home insurance quotes that are available becomes limited. As a result, you may not be getting the best priced policy.

Furthermore, carriers rely heavily on a post-bind inspection. This is a formal property review that happens right after your policy starts and sometimes before the next renewal. Between the overhead satellite data and the detailed post-bind inspection reports, insurers will easily spot any branches hovering too close to your house. If they flag your property as a high risk, they can choose cancel your policy during the initial underwriting period or non-renew your policy at expiration.

The Impact on Home Insurance Eligibility and Rates

Can trimming your trees really save you money? Yes, it absolutely can.

Better Eligibility: Many insurance companies in Texas will deny coverage or refuse to renew a policy if their satellite data shows overhanging branches. Trimming your trees keeps your home eligible for coverage in a tough market.

Lower Premiums: Many insurance providers offer better home insurance rates for homes with a roof in good condition and no overhanging trees.

Avoiding Claims: The cheapest claim is the one you never have to file. Keeping branches clear prevents costly claims, which helps keep your long-term insurance history clean.

How Much Should You Trim?

As a general rule, you should hire a reputable tree trimmer. Keep all tree branches at least 10 feet away from your roofline. This distance creates a buffer zone. It prevents branches from hitting your house during high winds and keeps pests like squirrels and rats from climbing onto your roof.

Let a Local Home Insurance Expert Help You Save

You do not have to shop for coverage completely alone. Reach out to a local independent insurance agent like AlphaSure Affordable Insurance Services. An independent agent can look at multiple home insurance companies at the same time. Thus, they will save you time and help find you the best rates for both your home and car insurance. Call AlphaSure Affordable Insurance Services today to start shopping for car or home insurance tailored perfectly to your budget. You can also go online for free home insurance quote to start the shopping process.

When you buy auto insurance in Texas, you might naturally focus on protecting your own vehicle. It makes perfect sense to worry about a dented bumper or a totaled car. However, many drivers make a major mistake during this process. They choose the lowest possible liability limits just to save a few dollars on their monthly premium bill.

Understanding Liability Coverage in Auto Insurance

What exactly is liability coverage? This crucial part of your auto insurance policy pays for property damage and bodily injuries you cause to other people in an accident. Currently, Texas law requires minimum limits of 30/60/25. This means that if you are at fault in an accident, your policy pays up to $30,000 for an injured person, $60,000 total for all injuries in one wreck, but not one person gets more than $30,000, and $25,000 for property damage.

These numbers might sound large at first, but medical care and new vehicles cost a fortune today. Consequently, if you cause a serious crash, you can easily blast past these minimum state requirements. For instance, if you total someone’s new $60,000 SUV, your minimum policy only covers $25,000. Therefore, you must pay the remaining $35,000 completely out of your own pocket.

The Real Danger Behind Having Low Liability Limits on an Auto Insurance Policy: Lawsuits and Legal Fees

Even worse, the other driver might decide to sue you for the remaining balance. A massive lawsuit brings expensive lawyers, courtroom costs, and endless stress. Ultimately, paying for a major legal battle is far worse than losing a cheap $2,500 car. If you lose the case, those mounting legal bills can drain your personal savings, spark wage garnishment, or force you to sell your assets.

Low liability limits put your entire financial future at risk simply to save a tiny bit of money today. Fortunately, increasing your coverage limits gives you peace of mind and shields your hard-earned money from sudden disasters.

Protect Yourself with a Local Car Insurance Expert

Do not navigate these complex choices alone. Call a local independent insurance agent like AlphaSure Affordable Insurance Services today. Independent agents compare multiple companies to find the best rates for your car or home insurance. They will ensure you get the protection you actually need at a price you can easily afford.

Imagine this scenario: You just filed a collision claim on your car insurance after a fender bender in downtown San Antonio. Your vehicle needs a week of bodywork, so you head to a local San Antonio rental car agency to pick up a temporary ride. You have a road trip planned down Interstate 35 to Laredo, but you stop and wonder: How does my Texas car insurance policy handle this rental?

Understanding how your policy moves with you is the best way to avoid surprise costs. Let’s break down how rental reimbursement works, whether it pays for physical damage, and if your coverage will follow you down to Laredo.

What is Rental Reimbursement Coverage in a Car Insurance Policy?

Rental reimbursement is an optional coverage add-on to your Texas auto insurance policy. You must buy this coverage before an accident occurs to use it. If your personal car is damaged in a covered collision or comprehensive claim, this feature pays for cost of a temporary rental car while your vehicle is in the shop. It will pay up to the limits shown your policy declarations page.

Texas policies typically structure this benefit with a daily limit and a maximum total limit per accident. For example, your plan might cover up to $40 per day for a maximum of 30 days. The insurance company pays the rental agency directly, or they reimburse you after you submit your receipts.

However, you must remember one key detail: This coverage only pays the rental agency’s daily fee, taxes, and basic administrative costs. It does not pay for gasoline, security deposits, nor any damage you may cause to the rental.

Will Rental Reimbursement Cover Damages to the Rental Car?

No, rental reimbursement coverage will not pay for physical damage to the rental car. Rental reimbursement only pays the cost to rent the vehicle up the policy limits shown on the car insurance policy declarations.

If you scrape a pole or get into a second accident while driving the rental vehicle, rental reimbursement will not help. Instead, your primary auto policy may step in to cover those physical losses. Refer to your policy or talk to a licensed agent about this.

Will Your Car Insurance Follow You to Laredo?

First off, it is very important to read your policy or talk to your agent. In general, your auto insurance coverage may follow you. When you pick up your temporary vehicle in San Antonio and drive south to Laredo, your liability coverage to others will cover the damages you cause to another party. Some policies, but not all, will extend physical damage coverage, comprehensive and collision to rental car minus the deductible.

For some car insurance policies, this information may not apply.

Nevertheless, here is how your primary car insurance policy may apply to that rental car:

Liability Coverage: If you cause an accident on the way to Laredo, the liability insurance portion of your auto policy will pay for the damage to the other driver’s car and any medical bills they incur.

Collision Coverage: If you hit a guardrail or another vehicle, your collision coverage pays for the physical damage to the rental car, minus your deductible. Once again, read your policy carefully. Some non-standard policies may not cover rental cars at all.

Comprehensive Coverage: If a sudden hailstorm damages the rental car while parked in Laredo, your comprehensive coverage will pay for the repairs, minus your deductible.

Watch Out for Rental Agency Fees

Your personal insurance policy may cover the physical damage of the rental, but rental car agencies often charge extra hidden fees after an accident. The two most common are “loss of use” fees and “diminution of value” fees.

Loss of use fees are assessed by the rental car company to cover the money the rental agency loses while their car is in the shop and cannot be rented to someone else. Diminution of value fee is assessed to cover the drop in the vehicle’s resale market value because it now has an accident history.

Standard Texas auto policies frequently do not pay for these rental car agency administrative fees. Because these fees are typically not covered by a car insurance policy, it is highly recommended to purchase a damage waiver directly from the rental car agency.

Let AlphaSure Affordable Insurance Services Find the Right Policy for You

Navigating the details of rental reimbursement coverage does not have to be complicated. When you are shopping for your next auto insurance policy, partnering with an independent insurance agency like AlphaSure Affordable Insurance Services gives you the advantage. Because we are independent, we work with multiple top-rated insurance carriers to find you the best coverage and rates for your specific needs. Whether you want to ensure your coverage follows you on your next road trip or you just need to update your existing policy, our local team is here to help. You can easily go online to request a quick quote, give us a call, or stop by to visit us in person at either of our convenient office locations in San Antonio or Laredo, Texas.

For most families living in Texas, a home is more than just a shelter; it is often the single largest financial investment they will ever make. Consequently, understanding the importance of having home insurance is critical for long-term financial stability. While no one expects a disaster, being prepared ensures that a single event doesn’t lead to a total loss of your hard-earned assets.

Homeowners insurance is a contract between you and an insurance provider that provides financial protection against disasters. A standard policy typically covers both damage to the property itself and your legal responsibility for any injuries or property damage you or your family members cause to others.

What Does Home Insurance Cover?

When evaluating policies, many homeowners ask, “What does home insurance cover exactly?” While every policy is unique, most standard homeowners insurance policies include four essential types of coverage:

Dwelling Coverage: This pays to repair or rebuild your home if it is damaged by a covered peril such as fire, windstorm, hail, or lightning.

Personal Property: Your furniture, clothes, electronics, and other personal items are covered if they are stolen or destroyed by a covered disaster.

Liability Protection: This covers you against lawsuits for bodily injury or property damage that family members or pets cause to other people.

Additional Living Expenses (ALE): If your home is uninhabitable after a fire or other insured disaster, ALE pays the additional costs of living away from home, such as hotel bills and meals.

However, it is important to note that standard policies in Texas usually do not cover damage caused by floods. Because the weather in South Texas can be unpredictable, discussing these gaps with an independent insurance agent is a vital step in your shopping process.

Why Work with an Independent Insurance Agent?

Choosing the right coverage can be overwhelming. Furthermore, rates can vary significantly between carriers. This is where the value of an independent insurance agentbecomes clear. Unlike “captive” agents who work for a single company, an independent agent works for you.

At AlphaSure Affordable Insurance Services, we serve as your starting point in the shopping process. We compare multiple top-rated carriers to find the coverage that fits your specific needs in both San Antonio and Laredo.

Are you buying a new or used car in Texas? Many buyers only look at the dealership sticker price. However, you must look at the total cost of ownership. Your car insurance premium makes up a massive part of this total cost. If you ignore insurance rates, you might end up with a monthly bill you simply cannot afford.

Therefore, researching coverage costs is vital. When you insure a vehicle, the insurance company evaluates its make, model, and year. Furthermore, they look at repair costs, theft rates, and safety ratings.

Let us dive into which vehicles from 2006 to 2025 cost the most and least to cover in the Lone Star State.

The Least Expensive Vehicles to for Car Insurance (2006–2025)

Generally, family-friendly vehicles and small SUVs cost the least to protect. Why? Because drivers usually operate them safely. In addition, they feature excellent safety equipment and use cheap replacement parts.

Here are the cheapest types and models to insure:

Small and Midsize SUVs: The Honda CR-V, Subaru Outback, and Ford Escape consistently offer great rates. These cars protect passengers well in crashes.

Minivans: The Honda Odyssey and Chrysler Pacifica rank as some of the cheapest vehicles to insure. Families drive them carefully, which leads to fewer accidents.

Rugged Off-Roaders: The Jeep Wrangler is historically cheap to cover. Mechanics can easily find and replace its parts.

New vs. Used: Older models, like a 2010 Honda CR-V, will cost much less to insure than a brand-new 2025 model. Older cars typically do not have modern aged technical components, like sensors. Consequently, this lowers the to repair a small fender bender.

The Most Expensive Vehicles for Car Insurance (2006–2025)

On the flip side, luxury cars, sports cars, and high-end electric vehicles will drain your wallet. These vehicles cost a fortune to repair.

Luxury Sports Cars: The Maserati Quattroporte, Porsche 911, and Audi R8 top the charts every year. They require expensive, imported parts and specialized labor.

High-Performance Muscle Cars: The Dodge Charger SRT Hellcat and Ford Mustang Shelby are very costly. Insurance companies know that drivers push these fast cars to their limits, which causes more severe wrecks.

Premium Electric Vehicles (EVs): High-end EVs, like the Tesla Model S and Porsche Taycan, carry massive insurance tags. They feature expensive battery packs and complex computers. Furthermore, mechanics need special training to fix them.

Why Texas Drivers Pay More for Car Insurance

Texas drivers face unique challenges on the road. We deal with destructive hail storms, busy highways in cities like San Antonio and Laredo, and a high number of uninsured drivers. Because of these local risks, finding a car in a low insurance bracket is even more critical here than in other states.

Conclusion

Before you sign any paperwork at the dealership, call an independent insurance agent like AlphaSure Affordable Insurance Services for free car insurance quote. Give them the Vehicle Identification Number (VIN) of the specific car you want. Getting a quote first ensures your dream car does not become a financial nightmare.